Xi “Limping” Jinping isn’t just a mass murdering dictator, he’s a control freak. (Limping, because China is limping from crisis to crisis under his “leadership”. More below the fold.) He has ambitions of empire, using “soft power” to expand the CCP’s control of other countries. But more and more he’s turning to hard power.

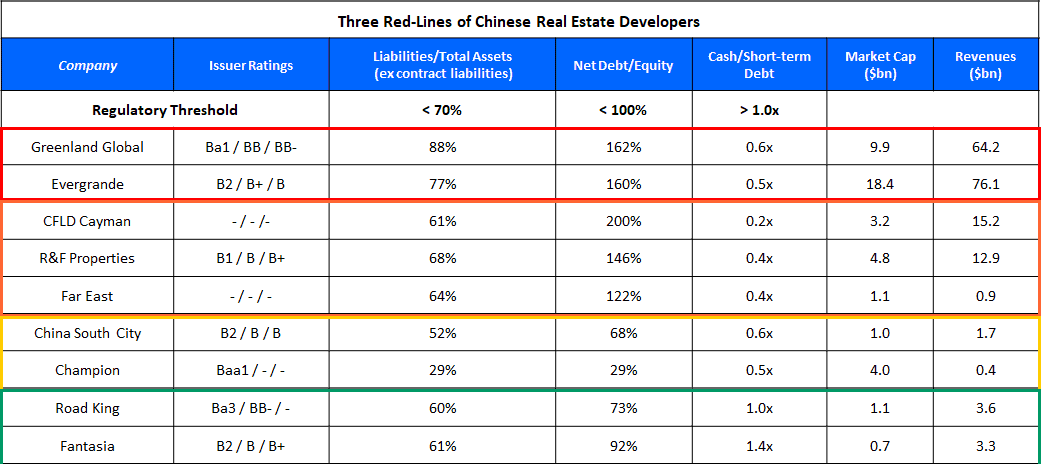

In August 2020, Xi enacted his “three red lines” policy to reign in the Chinese real estate market’s Ponzi scheme:

- Liability to asset ratio of less than 70%

- Net gearing ratio (debt v equity) less than 100%

- Cash to short term debt ratio of at least 1:1

More projects required greater debt financing, so prices went higher to cover those debts. But the disparity between loans and revenues kept growing, and the sources of revenue and suckers home buyers was starting to shrink. A collapse was inevitable. If the bubble wasn’t slowly deflated, it could collapse the country’s entire economy.

In spring 2021 the rumblings had started, and by August 2021, PRC citizens have stopped buying homes, not even tempted when real estate companies started dropping prices. One of the real estate industry’s primary source of revenue dried up, leaving them only with bonds to generate revenue.

But now, as we’ve seen in the last month, the companies can’t even pay their bond holders’ interest payments, let alone their debts. Real estate companies have very little cash on hand and now have three choices: finish building homes, pay off foreign creditors, or pay off domestic creditors. They claimed they would finish the homes, but instead paid off Chinese creditors and screwed over the little guys, just like wall street would. Evergrande has started trading stock again (dropping 14% value in one day) but said “No guarantees debts will be paid”. Who would put money into something that doesn’t promise to pay out?

Foreign banks and investors have stopped putting money into China. No one will buy worthless bonds, and domestic PRC banks aren’t likely to relend more money. All the real estate companies can do now is try to sell off assets to pay bond holders. But even those deals are starting to fall through, as DeutscheWelle reports in the video below. Why pay full price when you can wait for the fire sale auctions and pay pennies on the dollar?

So what will happen if these companies can’t pay their creditors? The US attitude has been “too big to fail” and used public money to bail out private corporations. The US does not believe in nationalizing anything, not even to pay back the taxpayers who footed the bill of american socialism.

I suspect Xi’s plan is to seize and nationalize these companies, just like Mao and the CCP stole land in 1961. Mao stole the land, lying that he would “redistribute it to the farmers” but in reality keeping it for the party while farmers remained sharecroppers. The real estate companies will weaken to the point that government takeover (seizure and nationalization) is the only way to prevent a complete collapse. It will allow Xi to exert even greater control over the country and the world’s economy, screwing over home buyers just like Mao did the farmers.

The fly in the ointment is that foreign creditors will still expect payment first. But when you’re a dictator, you can print as much money as you like. The question is, will foreign investors swallow that bait or cut ties and quarantine the economic mess to the PRC?

Click the link for the full story and the complete chart (the one below is abbreviated from that on the link). The PRC real estate companies are rated as red, orange, yellow and green in their relation to the “three red lines”. But the colours don’t mean much. Fantasia is listed as “green” yet it was one of the first to default and took its shares off the Hong Kong stock exchange to hide its losses.

Chinese Developers’ Bond Spreads Widen as Focus on Three Red Lines Increases

Another important factor that has come into focus is Beijing’s “three red-lines”. The three red-lines are a set of thresholds on three financial ratios, Liabilities (ex advanced proceeds) to Total Assets, Net Debt to Equity and Cash to Short-Term Debt, directed by the People’s Bank of China (PBOC) and the Ministry of Housing that cap developers’ borrowings. The measures were announced in 2020 and if a company’s three ratios are within the thresholds, its allowable annual increase in debt is 15% in the following year. The three red-lines currently focus primarily on large developers, the likes of Evergrande that breached all the metrics as of its last published numbers. To dig deeper into how the most popular developers are faring on the three red lines, we have listed the three financial ratios (based on last published earnings) for each of them in the table below, with issuers that breach all three red lines at the top and those that are within the thresholds of the three ratios at the bottom.

But things in Beijing aren’t all rosy.

Flooding in the country is worse in 2021 than it was in 2020, and food shortages are increasing. When even their own propagandist mouthpieces admit it, you know it’s dire. Dozens of dams have neared collapse, and the regime has had to flood vast areas downstream to alleviate pressure, sometimes blasting and destroying entire dams. Flooding hit cities where people drowned in subways.

China is suffering energy shortages because it can’t mine coal (thanks to the flooding) or get natural gas, and hydroelectric dams are shutting down. Cities in China are suffering blackouts that could be mistaken as being from North Korea. And it’s October. With energy prices soaring, mass deaths due to cold is a real possibility. Beijing saw temperatures below freezing last week, three weeks earlier than average.

China’s population is ageing thanks to the “one child policy” and selective abortion creating a gender disparity of 30 million more men than women of Millennial age. In desperation, the CCP has “legalized” having three kids and is now encouraging it. But that means nothing to young workers with no money, no homes, and no time.

Millennials in China have, whether just giving up or engaging in peaceful protest, started “lying flat”. The nearly slavery conditions of “996 jobs” (work 9am-9pm six days per week for the same wages that 9-5 Mon-Fri used to pay). They aren’t marrying, aren’t having kids and aren’t trying to buy houses because they know it’s hopeless. Tens of thousands now refuse to take more than part time work, making enough to live cheaply and no more. The lack of labour is so dire that the regime is using the propaganda machine to label those “lying flat” as enemies of the state.

Remember the “tofu dreg” problem of shoddy building construction? It may be the same problem in their tech sector. Spyware maker Huawei is being forced to use slow 4G chips in its phones not just because of the worldwide shortage or sanctions, but because domestic companies are producing inferior product. China is desperate to get a chip machine from ASML Holdings, which both the Netherlands and the US refuse to allow. China is years behind in semiconductor technology. Meanwhile, Taiwan’s TSMC is spending US$100 billion to increase production, though the effects will take years to reach the market.

The chip shortage will likely bring worldwide car production to a halt, but that’s not the only problem. There’s also a magnesium shortage in China, something needed for battery production and aluminium alloys in cars. China would like to control the world car market, but the regime needs to export magnesium for money and can’t mine it fast enough (again, due to flooding).

And “soft power” isn’t working. Thailand will stop using China’s vaccines once they run out because people who received the Sinovac or Sinopharm vaccines have needed a third booster shot. Two recent arrivals in Taiwan tested positive for COVID-19 despite having two Sinovac shots. Other countries are dropping China’s vaccines in favour of others. Meanwhile Taiwan’s Medigen is undergoing Phase III trials in Paraguay, results expected by the end of the year. The Lancet has published a peer reviewed article about the vaccine.

Speaking of COVID-19, who knows the real extent of lockdowns and spread of the Delta variant in the country? The latest outbreak is spreading right now.

Xi has ambitions of being a lifelong dictator. His purges in 2013 eliminated political enemies, and term limits for the general secretary of the CCP were eliminated, allowing him to copy Putin and Mugabe’s autocratic rule. But a winter of starvation, blackouts, and economic collapse could lead to a soft or violent coup. One was plotted in 2017 and snuffed out. But with the enemies he has made, his sabre rattling and decisions that could cripple the country, there may be enough support this time.

Oh, look, they’re re-inventing the errors of capitalism. It’s always so funny when Americans talk about how China is “communist.” Oh, really?

that is a fantastic rundown of the problems. an amazing shitshow.

I forgot to use Xi’s most common nickname.

Winnie the Pooh. Apparently, he hates it.

Unfortunately, a famous error of failing politicians is to declare a war somewhere to distract attention from the sinking ship back home. I hope that isn’t a strategy he uses.

Over here, we hear a lot about the great displays of loyalty people show towards him, but it all sounds quite performative. Does he actually have much support among, say, young people, or are they able to see right through his propaganda screen?

https://www.washingtonpost.com/world/asia_pacific/evergrande-china-debt-bond-payment/2021/10/22/eff0c986-2fd9-11ec-8036-7db255bff176_story.html

Evergrande somehow managed to make the payment today. At least China’s state news is reporting that Evergrande did and none of the bond holders have denied it. This is late but just inside the window for legal default. Everybody has refused to answer on how Evergrande came up with the money. The most likely option being some deal with China’s government, likely on terms very bad for Evergrande because they owe more money that they don’t have.

Isn’t “control” more or less the point of being a dictator?

Although I wonder how much control he really has? Much has been written about bureaucratic infighting in the CCP. Lots of conflicting interests and a lack of horizontal cohesion between different agencies.