France is experiencing unrest over President Macron’s proposal to raise the retiring age, when workers can start collecting their pensions, from 62 to 64 by 2030. Nationwide strikes have been called over this issue. As Kevin Drum points out, the unfairness of fixing by age when people can retire is true for the US too, because people whose work involves manual labor typically start work at an earlier age than those who go to college and get advanced degrees. Not only do the latter they put in fewer years of work, the work they do takes much less of a toll on their bodies and, crucially, they live longer.

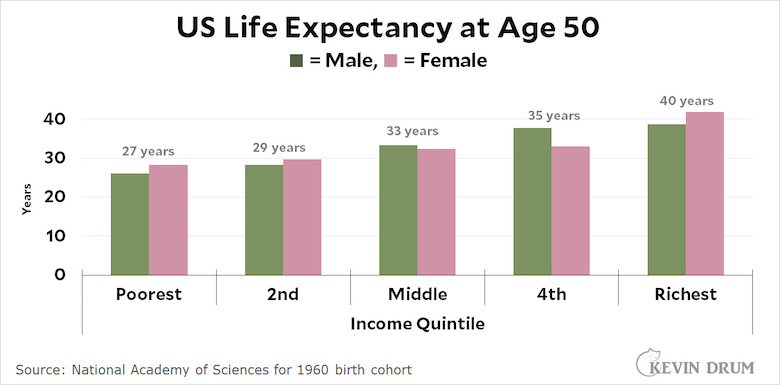

High-income workers work fewer years and live a lot longer than low-income workers. Here’s what that looks like for the US:

If you have 27 years of life left at age 50, you have about 15 years of life left at age 62. Cutting that by two years hurts a lot more than if you have 28 years left, as the rich do.

Hence while those who are richer may view raising the retirement age with some degree of equanimity, this is not the case for those who have worked much harder for longer.

Drum suggests that a different system that might adopted.

Instead of using a retirement age, for example, you could base pensions on number of years worked. As illustration, consider this simplified scheme:

- 45 years of work is the norm.

- Anything over 1,700 hours counts as a full year.

- Anything under is pro-rated.

- Your full pension is due when you have either (a) worked 45 years or (b) reached age 67.

So if you start work at age 18, you’ll get your pension at age 63. If you go to college and start work at 22, you’ll get your pension at age 67. The size of your pension will still depend (partly) on how much you contributed to the system in your working years.

NPR had a segment where they heard from some French workers about this issue, such as this man who works in a slaughterhouse.

“It’s extremely physical work getting these huge animals through the process,” he says. “No one will be able to do two more years under this reform – no one.” Mathieu Gallard is a pollster with Ipsos in Paris. He says 70% of the French oppose the overhaul of the pension system. That’s up 10 points from September. Gallard says respondents do not believe the pension system needs fixing. It had a surplus in 2021. And he says the French public thinks the burden will not be shared equally.

MATHIEU GALLARD: Emmanuel Macron has been seen as a president for successful people, I would say. And they tend to think that this reform will be a gain for – you know, for professionals and manager, but not for the working class.

The government consulted with unions over the draft proposal. It has provisions for those with physically difficult careers and night work. It raises the minimum retirement amount to 1,200 euros a month. And yet people are fixated on the retirement age.

…But Prime Minister Elisabeth Borne says working until 64 is nonnegotiable because workers need to pay into the system longer to keep it viable.

In the US too there are periodic calls by right-wingers to raise the age of eligibility for Social Security and Medicare and the objections to that move would be the same as for France’s proposals for raising the retirement age.

It’s an inescapable actuarial fact that people are living longer, which makes the system unsustainable.

I do get annoyed when I hear people trotting out the fact that they’ve “paid into the system all their lives” -- it betrays ignorance of how it works. Yes, you paid in, to cover the cost of the people who were retired already back then. Your pension will be paid by people paying in in the future… but there aren’t as many of those, and there are too many of YOU.

My grandparents’ generation all smoked and drank and fought a war, and bequeathed their children a social security and national health system that paid their fees AND expenses right through to masters-level education, paid for all their healthcare, paid them if they were unemployed, and paid for their housing. They then had the decency to work until they reached the state retirement age of 65 (or 60 if you were a woman, even though women live longer and statistically have less physically demanding or dangerous jobs), and likely die within a year or two having taken almost nothing out of the system.

My parent’s generation took all that, and retired early on full, final salary pensions. And because of the health system, they didn’t die off, they just kept on and on and on drawing their pensions and voting fucking Tory. Meanwhile they also stopped funding expenses for students, stopped funding fees for students, massively cut back educational spending at school level, privatised much of the NHS and railways and utilities and out-of-work benefits, and stopped final salary pension schemes.

And now, having royally fucked my generation, as a final fuck you to us they’re going to turn around and ask us all to keep on working for another two or five or ten years, because there aren’t enough young people paying into the system today to keep all the bastards who got the best of it in pensions unless us middle aged people don’t get to retire like they did.

Bitter, me?

1. I think everyone should be required to spend some time doing blue collar work. If you have to clean the toilets in a McDonald’s or gather up and reshelve hundreds of books at the end of the day like I do, you might be a little more considerate towards blue collar workers.

2. Remove the cap on Social Security contributions. Stop pretending SS is a piggy bank and acknowledge that it is a national welfare system. I want Elon Musk to pay $1 Billion per year into SS, as well as massively increasing his income tax, and the same for all the other billionaires out there.

3. Free medical care for everyone. No copays, no annual caps. But, no chiropractic and no homeopathy. ALL medical treatments must be tested for safety and efficacy including “natural” herbal and traditional treatments in order for it to be paid for by the government.

@2:

I once went for a job at a Honda factory. In the interview it was made clear that, although I was applying for an intermediate level engineer job, I -- like every single other applicant for a job there, be it cleaners, accountants, HR parasites, managers or whomever -- would spend the first two weeks of my job on a shift on the production line, bolting wheels onto Civics or whatever. This was intended to make clear to all employees what they were really there for.

@1: “It’s an inescapable actuarial fact that people are living longer”

Only in some places and for some cohorts. In the USA (“Working our way toward the glorious 19th century”), some cohorts have seen a decline in life expectancy in recent years. Yeah, and I never thought I’d ever live to see that happen.

And Kevin Drum can stuff his “simplified system”. US workers are considerably more productive than they were in the 1970s yet their real income has been flat. All of that increased productivity has been hoovered up by the top few percent. People are working longer, with fewer benefits, and increased precarity, and Drum thinks it’s perfectly fine to have a retirement at 67 or 45 years of work (meaning that someone who went for an advanced degree will be working until at least 70, unless you count being a student as qualifying work)? Eff him. Raising the “normal” retirement age in the US from 65 to 67 was yet another way Reagan effed over the average American, all while smiling and waving at them. The bastard.

jimf @4, those who go into grad school or immigrate at an age later than 22 retire at 67 regardless of how many years they work, according to Drums system.

Warren Buffet has argued that Social Security can be made sustainable through three simple fixes. (https://www.fool.com/retirement/2018/05/21/how-warren-buffett-thinks-we-should-fix-social-sec.aspx):

1. Eliminate the taxable earnings cap.

2. Increase the payroll tax rate.

3. Increase the retirement age.

It is important that we have an informed national conversation on Social Security and its value to the health of the nation. I have been alarmed by proposals to privatize the system, to sundown it (every five years or annually), to cut benefits, and to raise retirement age. It is my understanding that implementing the first two proposals listed above would be sufficient to make the system sustainable and beneficial.

@1

“My parent’s generation took all that, and retired early on full, final salary pensions. And because of the health system, they didn’t die off, they just kept on and on and on drawing their pensions and voting fucking Tory. Meanwhile they also stopped funding expenses for students, stopped funding fees for students, massively cut back educational spending at school level, privatised much of the NHS and railways and utilities and out-of-work benefits, and stopped final salary pension schemes.”

Similar here in the States, not that we’ve ever had a proper health system. I’ve been workshopping (meaning discussing it with folks at the bar,) the idea that once you’re old, say drawing Social Security or some other criteria, you no longer can vote. I’m in my late 50s, no retirement in sight, and am more than tired of hearing my parents’ cohort (all retired at 62-65,) talk about all the health care they’re receiving, and whinging about the occasional $5 fee, while the bastards most of them voted for have made it impossible for me to have health insurance, and now are trying to take my Social Security.

Let the people who have a future decide on what the future should look like.

mikey:

Or, in other words, “retired people have no future”.

Nice sentiment, that.

Never vote for anyone who wants to take away voting rights. They don’t really care about our collective futures either, just that they get to have it their way (right now), no matter the cost (later).

But if you’re at (or well beyond) retirement age, you should consider retiring. Obviously, but apparently it has to be said. This means, among other things, that you don’t run for office, which amounts to a bunch of serious responsibilities that you may not be capable of fulfilling.

It is not just some prize to be won that you can brag about to your rich friends, nor is it something to which you’re entitled. It is work, which you may or may not be doing, depending on whether voters can come up with anyone better for the job. What it shouldn’t depend on is whether you were ever even interested in doing any actual work for the people you claim to represent in the first place, because that part isn’t supposed to be optional.

The problem is not just physically demanding jobs. Something like one seventh of people at age 65 in the U.S. have mild cognitive impairment or worse. Raise the retirement age and society ends up with more partially (mentally) disabled people in the work force. Or, employers fire and refuse to hire older workers. Then, many old people are no longer employed or employable but are not old enough to qualify for retirement benefits.

I think it’s simple as.

Basically, make retirement optional once the criteria are met, just don’t make it mandatory. Better still, give them tax breaks if they do work.

Many people are more than competent (and very experienced!) in their 60s, and advanced economies have lots of work for people who don’t need to be physically buff. They can be very productive.

Also, demographic pyramids. Or, as it seems, demographic time bombs.

Anyway, stupid to not allow people who wish to work for whatever reason to do so without penalising them if they don’t choose that.

Why does women’s life expectancy fall below men’s for the middle and 4th income quintiles?

@ John M, #11,

Things may be different in Oz, so I don’t fault any lack of knowledge you might have about how USA Social Security retirement benefits work. But maybe a few quick notes are in order:

1. Not everyone is eligible. To earn credits a person needs to be employed for at least 40 quarters with an employer who takes money for social security out of the employee’s paycheck, and pays additional money from company funds. Note a couple things about this. First, there is an argument which can be made that the money paid directly as a tax on the company accounts could go to increased employee wages if it wasn’t collected. This is a poor argument, as employer’s generally are not particularly generous with wages and would probably just keep that money for themselves. But you will see this argument made on occasion by small business owners who are being somewhat disingenuous. Second, employer’s who pay employees under the table are not collecting the social security money from their employees and/or not paying their share of the employee’s social security tax. So someone could work for a long time, not reach the 40 quarters (10 years) of employment, and not be eligible for social security retirement payments. When I started working, doing farm-work at the age of eleven, none of my income was claimed for taxes including social security. The first job where I started contributing to social security was when I joined the Air Force. I wasn’t hurt by the under-the-table payments, but there was the occasional farmhand who was in their 30s who was also not garnering their social security quarters. There are other programs run by the social security organization which can help people who cannot collect social security retirement, but there are people who cannot collect the US social security retirement funds. Needless to say, these are generally people who are already poor.

2. Retirement is optional in the US. You can continue to work as long as you want, and even collect social security during that time. While there is a sliding scale of payments based on the months around the base year, there is a maximum payment which can be reached. Note that once a person’s total income level reaches a certain threshold the social security payments start to be taxed, but it never goes away altogether.

3. Social security retirement payments are optional. You have to apply to the government to start collecting them. I’ve never run into anyone who doesn’t.

4. The amount of money each person gets for social security retirement payments is different for every person. It is calculated from the highest 35 years of earnings. People who have earned a higher total amount of money over those 35 years get a higher social security retirement payment. I’ve done pretty well, having worked my way from Technician to Chief Engineer, and I’m eligible for about $3,300/month when I reach the age of 67. My wife never got higher than a secretary position, and has had a number of years where her earning are zero, so her benefits are about $900/month when she reaches the age of 67. I could retire at the age of 62, and if I do so my social security retirement payment would only be around $2,200/month. Five more years of work means an extra $13,000 a year. I still may be able to retire at the age of 62 if my other investments are doing well, and I will be the first to admit that the money I get from social security retirement payments will be higher than that of a lot of other people. That may not be fair, but that’s the USA system. There is one big reason why I may not be able to retire as soon as I’m eligible, and that is point 5.

5. Health care. Medicare starts when a person reaches the age of 65 (and there are limited windows for signing up for Medicare so if you miss the window one year you have to wait for it to open some months later). Someone who retires at the age of 62 needs to purchase health care insurance for the three years between the time they leave employment and the time the are eligible for Medicare. And the health insurance for that period is not cheap. First of all, the insurance companies know that they will only collect income from the person for a short time, and they also know that someone in their sixties is more likely to need expensive health care then someone in their thirties. So a lot of people will work three more years in a job they might otherwise retire from in order to keep health care. Now a person can get an extension of their last employer’s health care policy through a program known as COBRA, which is intended to help bridge any gaps between employment. But that has a limit of 18 months (36 months in some special cases). It also means that the person would be paying the entire monthly healthcare insurance bill out of their own pocket, but it’s a lot cheaper than getting a new policy at the age of 62. So if I wanted to avoid having to pay through the nose for healthcare insurance, I could retire at the age of 63.5 and use COBRA for 18 months. Except that my wife is on my employer’s insurance with me, and she is 15 months younger than I am. So, to ensure that her medical bills are at least partially covered I would need to go on COBRA three months before my 65th birthday. Basically the same time I would need to apply for Medicare.

But, you can work as long as you like. There is no mandatory retirement in the US. Some people have to keep working into their eighties, even if they don’t want to, because of the huge holes in the social safety net in the US.

I would like to add one clarification to flex’s excellent explanation @13: Another option people in the USA have is to stop working at some point, but delay collecting benefits until later. The reason to do it is that the benefits are higher if one starts collecting later, up to age 70 when they reach the maximum (so no point in delaying beyond that). This of course only works for people who have some other source of income besides work (say, investments or rental property, or the income of a spouse). This is yet another way the system benefits those who are relatively well off. Benefits starting at 70 are about 24% higher than benefits starting at 67.

Oh, and regarding a couple such as flex and wife: If the spouse with the higher benefits is already collecting benefits when the spouse with the lower income applies, the spouse with the lower income may get an additional benefit so that together that spouse’s benefit is 50% of that of the higher earning spouse.

Thank you both, that’s informative.

I found this ‘game’ where you can try to find a combination of policies that would make US Social Security solvent for longer.

In this blog post there is discussion of how to make Social Security solvent for a very long time by slowly raising the payroll tax, The author doesn’t like making the rich pay more because that would give the rich more legitimacy to design how Social Security is run FDR already made the point that Social Security not be seen as a welfare program, which the rich don’t like and want to cut all the time.

Part of the strategy for years from the USA republican party has been to re-brand social security as a welfare program. The first step they want to take is to institute “means-testing”, which basically says that if people already have an income (from investments/rents/etc.) that means they don’t need social security. This will be sold as a way to keep social security solvent, and it will probably sound reasonable to a lot of people, including a lot of democrats. It will sound like it’s a fiscally responsible thing to do, and that it will also hurt the wealthy.

However, this tactic is a wedge, once means-testing is introduced then the social security retirement payments become much easier to define as a program for poor people, as a welfare program, and it will allow congress to continually adjust what income level gets benefits. It also opens the door for other restrictions to divide the population and remove chunks of people from social security one bite at a time. There is a reason why the social security retirement benefits is given to everyone who worked. The reason is to make it more difficult to strangle. If everyone gets the benefit, it can’t be called welfare. Once it becomes a program for a subset of the population, and a poor subset at that, it becomes much easier to kill entirely.

Many years ago I was at a party with Representative John Dingell, and was present during a conversation where the problems with social security running out of money was discussed. [I was an elected official at the time, and it was John’s annual Christmas party, but I wouldn’t claim to know him. A lot of local elected officials were invited to his parties and you went to be seen, not because you were going to have an extended conversation with your representative. I did a lot more listening than talking.] Rep. Dingell kind of laughed about the problems with social security solvency, because he was present during a previous social security funding problem which occurred in the mid-nineteen nineties. Congress had delayed re-structuring the financing of social security to the point where payments to retiree’s would stop within two days. They literally had only a few hours to work out a compromise to keep the checks running. They managed it, although the compromise only kept the program fully solvent until the 2030’s. Even at that time there was a proposal to remove the cap on the amount of wages which would be subject to the social security tax, because that would keep the program solvent in perpetuity. But there wasn’t support from the republicans needed to pass the bill for that proposal, and it was dropped.

The USA social security retirement income program is not fair and has a lot of holes, it should really be scrapped and rebuilt as a guaranteed supplemental income program. It was built as a compromise, weighted toward people who accumulate more wealth during their working lives, and has been jury-rigged to keep it going ever since. Any changes to it will require that those people who are already getting benefits don’t see a reduction, which automatically means a headwind opposing change.

(OT Note: I had learned previously that “jury-rigged” was a debased form of a more derogatory term “jerry-rigged”, stemming from the use of the term “Jerry” for a German by the British in WWI. However, it appears that what I learned was incorrect. According to a Merriman-Webster article, the term jury-rigged dates back to the 15th century, from the Middle English term “jory”, which means an improvised, temporary, sail on a ship. Of course the “rig” part of jury-rigged also refers to the lines used on a sailing ship, so “jury-rigged” really means a ship outfitted with a temporary sail from makeshift components (possibly the clothing of the sailors). It doesn’t necessarily mean shoddy or slatternly. I find it fascinating that some phrases survive for so long.)