In 1999, I became a millionaire on paper by selling shares in a company that I had created for the express purpose of selling the shares. That ought to sound bizzare to you, and it is – it’s one of the weirdest parts of corporate capitalism. The entire thing feels like a scam, except that the money is very real, or it’s not, depending on what happens.

This posting may help you understand Marx’s dialectical reasoning, too. Marx, in Capital, is trying to explain why things are worth what they are. This was crucially important to Marx for two reasons: 1) for political reasons he was trying to develop a theory of what labor was worth so he could argue precisely how badly industrialists were screwing their workers, 2) economics doesn’t make sense without a theory of value to explain why anyone pays anything for anything. If we don’t have a theory of value, everyone just turns to market value: what is someone willing to pay for my thing?

Suppose I have a dozen bananas and Kent Hovind wants to buy one. He asks me “how much for a banana?” and I reply, “for you, $100.” He says “that had better be a good banana!” and I reply, “it was made by god.” And he forks over $100 and I give him the banana. We have now established a market price for bananas: $100. Of course someone else might come along and offer me $.05 for a banana (and I’d take it) – now what is the value of a banana? We can see that it’s got a market price that’s fluctuating in a certain range, but we just don’t have enough long-term data to be able to price the banana. [If we had long-term data we might base our notion of the value of a banana on the long-term average market price.]

Now you can see why being able to value a banana would be important to Marx: a worker who collects bananas in horrible, hot, brutal conditions, has helped produce the valued item. If we’re selling bananas at $100 and an exploitative capitalist is paying his (it’s always a “him” isn’t it?) workers $1/1000 that they pick, we’re justified in calling them “exploiters.” If bananas sold for $100 apiece and we’re paying the worker $5/banana I’ve probably put myself out of business because – while I was being generous to my laborers – I forgot to account for shipping, packaging, bribes, duties, taxes, and whatnot.

Aside from the absurd price-structure I made up for bananas, that’s about how it works in capitalism. My farm and my banana trees and my infrastructure costs are the means of production and Marx was trying to tease of the relationship between what happens when labor doesn’t control the means of production, and capital can use their control of production as a weapon against labor. I.e.: Andrew Carnegie could threaten to shut down the Homestead steel mill for 6 months because he knew the workers would (literally!) starve and – while he’d lose money not having the mill working – he’d be the last man standing. Andrew Carnegie was exactly the kind of son of a bitch that would do that; it’s how he got to be so incredibly rich.

Capitalism is blood sport. Marx was trying to establish a framework for understanding what things were worth because otherwise all anyone could do is shrug, “A banana? Last time someone sold a banana it went for $100.”

Now, we can talk about what a company is worth. You might be thinking, “it’s going to be worth how much it has in the bank, plus the total fair market value of its assets, plus maybe a million dollars for its brand identity, and the genius executive team that have been driving it to success are also an intangible asset but definitely worth something.” That is what you might think. But you’d only think that if you had not been paying attention. The company is worth whatever someone is willing to pay for it.

Perhaps you have heard the term “market cap” which is hip Wall Street-ese for “market capitalization” – what the market is willing to pay for a company. The market cap of a company is the total number of shares that have been issued, times the price per share, minus the company’s debt if any. If you think about it, you can see that any other calculation of its value is going to get fractally complicated: every asset that a company has, from post-it notes to nebulous “intellectual capital” has to be costed out and argued over. Instead, you just look at the market:

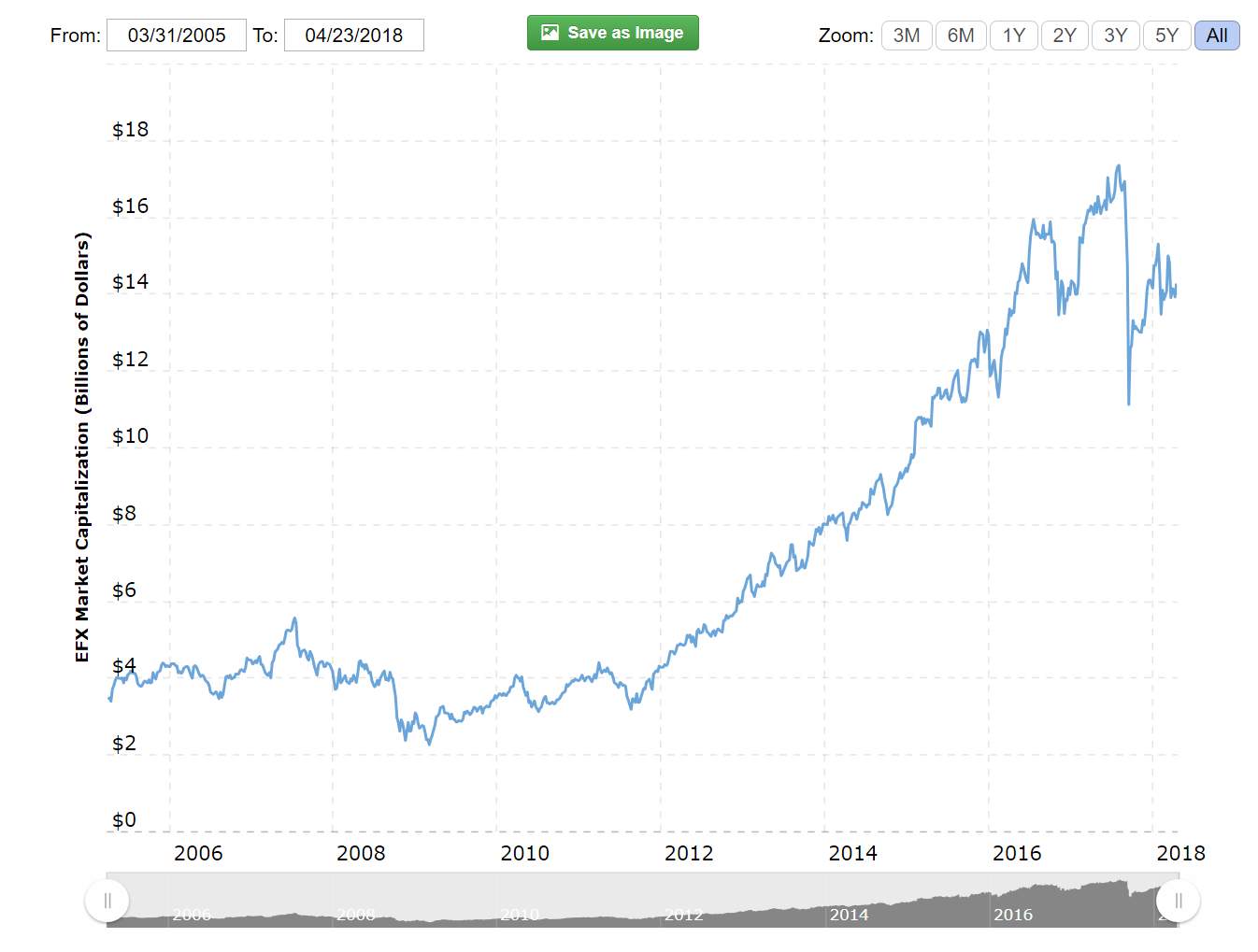

If you were an asset stripper, and you were thinking of buying Equifax and breaking it apart, it was “worth” $17 billion until the data breach was publicized, and the next day Equifax was worth $11 billion. There’s blood in the water! They may have just become affordable.

There are complications, of course: you don’t simply buy all the shares of a company and say “it’s mine, now! Bwaaahaaahaaa!” As you started buying up the shares, the share price of the remaining shares would go up (supply and demand!) as the Wall St gnome who trades the shares for that company adjusts the share price to reflect what someone is willing to pay. That, by the way, is called a market-maker: literally, the guy who sets the share price.

Remember the scandal where bankers were found to be rigging the price of the London Interbank Offered Rate (LIBOR) [wik]? Basically, the market-maker for a certain loan-rate decided to make very small fluctuations in the market price: a little lower for his friends, a bit higher for German banks – that sort of thing. The whole thing seems a bit odd to me, since the market-maker is basically an intermediary who has placed themselves on top of the money-spigot and they swear up and down that it would never occur to them to cheat even a tiny bit. And, with the amounts we’re talking about, a tiny bit of jiggering alters downstream prices by billions of dollars. The capitalists, and their regulators, smoke expensive cigars and drink heavenly rare whiskies, and pretend vigorously that the game is not rigged – which is weird because their entire job (other than to wear bespoke clothes and look good) is to rig the market. That’s what a market-maker does: rigs markets.

Now I can explain how I created myself a bunch of paper wealth out of thin air. I started a company! This was not some scam – I devoted 5 hard years of my life, 100%, to building my company. How a start-up works is: you start the company, issue a number of shares – let’s say 1 million shares – and then sell them to raise operating capital! The founders of the company write business plans and presentations and go and meet with venture capitalists and rich golf-playing douchebags who still wear those 80s gold ‘macho horn’ jewelry and very expensive suits. The business plan has to be good, practical and the idea has to be good, or good-ish and ideally it shows a path toward massive profit and global domination. Every start-up’s business plan is ridiculously hyper-optimistic. Except for the ones I wrote, which were down to earth, practical, and had achievable budgets and waypoints. I used to tell prospective investors, “this is not pie in the sky: look at these numbers and you’ll see I didn’t make them look exciting to get your money, because I know that I’m going to have to deliver on this and it needs to be real.” That bit of macho-humble posturing usually worked pretty well in the 90s but apparently it doesn’t work so well in 2017. I got involved in a start-up last year and we had real trouble getting the money because everyone wanted to know why we weren’t “doing blockchain big data yumyum facebook billion dollar exit?”

Now I can explain how I created myself a bunch of paper wealth out of thin air. I started a company! This was not some scam – I devoted 5 hard years of my life, 100%, to building my company. How a start-up works is: you start the company, issue a number of shares – let’s say 1 million shares – and then sell them to raise operating capital! The founders of the company write business plans and presentations and go and meet with venture capitalists and rich golf-playing douchebags who still wear those 80s gold ‘macho horn’ jewelry and very expensive suits. The business plan has to be good, practical and the idea has to be good, or good-ish and ideally it shows a path toward massive profit and global domination. Every start-up’s business plan is ridiculously hyper-optimistic. Except for the ones I wrote, which were down to earth, practical, and had achievable budgets and waypoints. I used to tell prospective investors, “this is not pie in the sky: look at these numbers and you’ll see I didn’t make them look exciting to get your money, because I know that I’m going to have to deliver on this and it needs to be real.” That bit of macho-humble posturing usually worked pretty well in the 90s but apparently it doesn’t work so well in 2017. I got involved in a start-up last year and we had real trouble getting the money because everyone wanted to know why we weren’t “doing blockchain big data yumyum facebook billion dollar exit?”

Anyway, I take those million shares and sell 333,333 of them for $2 million. That means my company is now worth $6 million! Which means that the 666,666 shares I still own, they’re worth $4 million!

Capitalists negotiating a start-up’s market cap with the founder.

Or, maybe I can’t sell the shares for $2 million. I guess the company wasn’t worth $6 million after all. Oops. Then, some venture capitalist says “I’d pay $1 million for it.” And, if I take that deal, my company is worth $3 million.

There’s another important concept, and that is liquidity. An asset is said to be “liquid” if you can convert it to cash easily and quickly. Let’s imagine you have a suitcase of Mexican Flake cocaine: that’d have a street value of about $1 million, cash. Contrary to what we see in movies, very few people walk around with that kind of money – so you have a liquidity constraint. When you create a start-up and sell those shares, you’ve suddenly created some paper wealth, but it’s less liquid than that suitcase of cocaine: its value goes to zero if you start trying to sell it because then your investors realize you’re trying to sidle toward the door. And then, it gets ugly. If you think some cartel boss is going to get mean because you stole that suitcase of cocaine, Wall Street gnomes are more vicious because they’re cowards. The cartel boss will kill you horribly because it’s business. The Wall Street gnomes will blacklist you and you would have no chance of getting a loan to open a taco stand, even if you put your house in the Hamptons up as collateral.

If you think the whole Donald Trump/Stormy Daniels affair has a great deal of lawyers involved, it’s not any different from a corporate financing deal. When you sell shares in a start-up, your investors are going to come along with stacks and stacks of requirements, basically none of which are negotiable. Why would they negotiate? They already know the market value of your soul. Those requirements are things like that if you try to sell an option on your shares, they get the money. If you quit, they get your shares for what you paid for them (usually about a dollar for those 666,666 shares) and if they fire you, you may have to forfeit some percentage of your shares, etc. This is called golden handcuffs, in the sense that the guys in the knife-fight are handcuffed together: they can be gold or they can be stainless steel, either way you’re not going anywhere.

Red in tooth and claw.

Next time I guess we’ll talk about stock options and maybe short-selling. Eventually we’ll talk about derivatives and we’ll all walk away from the discussion shaking our heads and going “WTF?! They imagine money, and it has value!?”

Marx dialectical reasoning: (I hope I don’t botch this!) in economics there are often propositions that change while you try to pin them down – for example, the price of a banana. If you keep asking me “what do you want for your banana?” eventually I am going to conclude that you are really interested in bananas and I’m going to creep my asking price upward. So, the thing we are examining – the price of bananas – changes as we examine it, because we examine it. In a sense, the price of bananas is a shared fiction between us. Marx’ dialectical method is a way of acknowledging that shared fictions between us are subject to change as we discuss them, so we will define things in terms of each other and in terms of how we discuss them. In that sense, it’s a great big circular argument, but it’s necessary. “What is the value of money?” can only be answered dialectically – literally “as part of a dialogue” between the parties involved. It’s a practical attempt to respond to linguistic nihilism.

There are further complications that have been bothering me for a while now… One that’s really been on my mind is the fact that everybody with a pension fund (or 401(K), or whatever the local equivalent may be) is essentially forced to buy into the market, and that money has to go somewhere. But it’s not like the sorts of companies that pension funds like to hold are issuing new shares every day… So you have god-knows-how-much money pouring into the market every month, and it’s all chasing the same assets.

This is even further complicated by the current vogue for “passive” funds, aka “index tracking” funds… The way you construct an index tracker is (in principle) simple – you buy every share on the index, in proportion to their weight in the index. So if you’re tracking the Marcus100 index, and BadgerCo comprises 10% of the total market capitalisation of the Marcus100, you put 10% of the money into BadgerCo.

Now, how the hell does that work with an “open-ended” fund – i.e. one where there is no hard limit on the amount of money invested in the fund? Again, running an open-ended fund is supposed to be simple – when people come along with more money they want to invest in your fund, you just buy more of the underlying assets and issue them new shares. However, if you’re tracking the Marcus100 index, that means you need to put 10% of whatever they want to invest into BadgerCo shares – but BadgerCo isn’t issuing any new shares. The only way you can fulfil your objective is by bidding up the value of existing shares. Thus, the market capitalisation of BadgerCo ends up having very little to do with the assets, liabilities, or activities of BadgerCo, and rather more to do with how many people want to invest in funds which track the Marcus100 index.

I have long suspected that this is about the only thing keeping the market afloat, and that that is a significant factor in the push to move people from bond-backed company pension schemes to market-based private pension schemes over the last few decades.

I remember when I was doing the move-out-of-town schtick and was selling my refrigerator for half price. It was only 3 years old, so that was a darn good deal. I ran an ad in the local paper (that’s how long ago this was)? Some woman called me to ask some questions. Then a bit later, her boyfriend called. He was the type who wants to negotiate everything. The annoying type. I told him no, the price wasn’t budging, and please don’t call back because I’d rather dump it in the harbor than sell it to you.

Dunc@#1:

One that’s really been on my mind is the fact that everybody with a pension fund (or 401(K), or whatever the local equivalent may be) is essentially forced to buy into the market, and that money has to go somewhere. But it’s not like the sorts of companies that pension funds like to hold are issuing new shares every day… So you have god-knows-how-much money pouring into the market every month, and it’s all chasing the same assets.

Yes, the market appears to have become a self-licking ice cream cone. More money pours in which makes it worth more and makes more money pour in.

I believe the term is “correction” – that’s when the market goes, “wait, no, bananas are not worth that!” and shrugs the price of bananas. Then, some of the banana sellers lose their shirts. Oddly, the market-makers always come out making money on both the rise and the fall (because the market-makers arranged it that way) so it’s all OK. For the market-makers.

Now, how the hell does that work with an “open-ended” fund – i.e. one where there is no hard limit on the amount of money invested in the fund?

It can buy derivatives! The cool thing (or the terrifying thing) about derivatives is that they are new valuable assets created out of thin air, so they don’t fluctuate until someone makes them fluctuate. Most pension funds stay away from derivatives because they are the financial equivalent of meth-covered cocaine sugar pops.

I may have this wrong but if I understand it, the indexed funds are trying to keep a certain percentage of their overall portfolio in a certain type of assets. So if I am trying to be a “50% banana businesses” portfolio, I can buy banana business shares at whatever price as long as I balance the portfolio to 50% bananas. So, the more I plow in there, the more I have, and if my buying a lot of banana stocks makes bananas go up, I re-balance into mangoes.

It’s also not super precise, because of market fluctuations. So the banana fund would be more or less 50% bananas at any given time, but we would accept the assumption that it would never be exactly 50% bananas because that’s a rapidly moving target.

Reginald Selkirk@#2:

I told him no, the price wasn’t budging, and please don’t call back because I’d rather dump it in the harbor than sell it to you.

That is a good case-study in “how not to dialectics.”

If you ever want to make someone like that’s head explode you can manipulate the dialectical overton window:

Guy: “How much is your fridge?”

You: “It says here, $200”

Guy: “Can you come down in price?”

You: “It says here, ‘$200 firm’ – which means I want $200 and am not prepared to lower the price.”

Guy: “But everyone haggles. Surely you have seen Monty Python’s Life of Brian? Haggle with me.”

You: “Very well. How about $199.99?”

Guy: “That is ridiculous. I was thinking more like $150.”

You: “$199.98 might be OK. But I don’t see any ‘7’ digits in the landscape of possibilities.”

Dunc@#1:

Thus, the market capitalisation of BadgerCo ends up having very little to do with the assets, liabilities, or activities of BadgerCo, and rather more to do with how many people want to invest in funds which track the Marcus100 index.

That, by the way, is part of why the whole system is so weird. We are inclined to assume that the price of BadgerCo has something to do with the value of BadgerCo, but if we did, we’re mistaken.

Think about it this way: Equifax loses $2 billion in market cap, overnight. But did the value of Equifax actually drop? It still has the same assets and liabilities. In fact, Equifax signed a big contract with the IRS right after the breach announcement made their stock plummet. We might imagine that Equifax got more valuable rather than less valuable.

Karl Marx was a very very smart guy, and very brave, to even begin to attempt to systematize this mess. I found it helpful to keep him in mind in the overall context of industrial capitalism and the abuse of labor, in order to understand the importance of what he was trying to do: he was trying to make a moral argument hidden in an economic argument based on a dialectical approach to establishing value. I usually just want to run screaming out of the room when I try to make sense of it.

I think you’re exaggerating the divorce between asset value and market value a bit. Firstly, for listed companies, they’re required to disclose a certain amount of information (and, to keep things fair [note 1], people with more information than what’s disclosed to everyone are not allowed to trade the shares).

Secondly, the problem of open-ended funds affecting markets when growing and shrinking is real, but less acute than you assume. The Marcus100 index includes shares in the top 100 companies in Badgeria by market capitalization; they’re big and have many shares and many people trade them. If BadgerCo is currently trading at $42 a share, you may not need to offer to pay more than $42.02 a share for oodles of people to want to sell them to you and bag the two cents.

(Incidentally, that’s how market makers are supposed to make their money [note 2], by being there to buy or sell stuff when a counterparty is not immediately on hand. Want BadgerCo shares? They’re $42.02 for you from the market maker, unless there’s someone selling them right then at $42.00, in which case you bypass the market maker. Have some BadgerCo shares to sell, and there’s no buyer ready? The market maker will have them for $41.98. The theory is that the market maker gets to keep this small difference in return for offering liquidity to customers.)

My point is that, if the holdings of the index-tracking fund don’t vary hugely, the amount of shares they need to trade is small, and unlikely to affect the market. They don’t have to trade it all at once — they can spread their trades over hours or days, to disturb the market even less. And it’s you, the investor, who pays this cost of getting in and getting out of the fund anyway. [note 3]

Note 1: bwahaha.

Note 2: see note 1.

Note 3: see note 2.

cvoinescu@#6:

I think you’re exaggerating the divorce between asset value and market value a bit. Firstly, for listed companies, they’re required to disclose a certain amount of information (and, to keep things fair [note 1], people with more information than what’s disclosed to everyone are not allowed to trade the shares).

Yes, that’s true. There is certain information (sales, bookings, acquisitions, new opportunities) that are disclosed, which may alter the market’s perception of the company’s value. That’s really all that anyone has to go on, other than profits – which is another interesting problem since the internet era, where you have public companies that are leaking money like Niagra Falls “leaks” water. Traditionally the market might value a company based on a multiple of revenues, but that model completely breaks down if your revenues are negative numbers.

If BadgerCo is currently trading at $42 a share, you may not need to offer to pay more than $42.02 a share for oodles of people to want to sell them to you and bag the two cents.

Yeah, I think that was exaggeration for effect. An individual can’t move a market very much, if at all. What moves markets are big buys – like if KKR starts trying to buy gigantic blocks of stock to get a controlling interest. Then the market will react because basically they can see something is up. In that sense it’s like those card games where there are acceptable signals that amount to formally approved ways of cheating. Insider trading is un-approved forms of cheating, but KKR starting to buy big blocks of stock in a company, and everyone jumps on, that’s just the market.

My point is that, if the holdings of the index-tracking fund don’t vary hugely, the amount of shares they need to trade is small, and unlikely to affect the market. They don’t have to trade it all at once — they can spread their trades over hours or days, to disturb the market even less. And it’s you, the investor, who pays this cost of getting in and getting out of the fund anyway.

I should have emphasized that; you are correct. It takes a big kick to move a market. Usually. (Or you get a panic sell-off or a bubble buy, which are the market moving dramatically because of a rumor or people trading along with a big player.)

There are other – worse – things that funds can do with how they spread their trades. I should probably explain how Hillary Clinton made so much money on the options market… But that’s for another posting.

The Zuckerberg Uncertainty Principle.

I should add that what I said is true for index-tracking funds, which do stick to the formula of the index very closely, so when a guy invests their retirement fund in them, they really have to go out and buy a few dozen shares of each of the 100 companies in the Marcus100 index.

Managed funds (the kind with a guy who decides what to invest their clients’ money in) can, and often do, hold large chunks of specific companies. If the manager suddenly decides they don’t like BadgerCo anymore, they can kill its value by trying to sell all those shares at once. Needless to say, they don’t normally do that, but it’s very hard to unload even a few percent of all the shares in a company; a larger chunk may take weeks or months. There are good-paying jobs in designing algorithms that try to hide the buying or selling pattern when a fund tries to trade a huge number of shares like that.

@#4

I just googled for it and watched the video. That was hilarious.

Reginald Selkirk @#2

Whenever I’m selling something, if somebody contacts me and starts haggling, I get mildly irritated—the person just wasted a bit of my time. When haggling, people usually say things like “there’s a defect here” or “there’s this thing wrong with what you are selling” or “this stuff isn’t worth as much as you are asking.” Hearing these kinds of words makes me think, “If you don’t like this thing I’m selling, why the fuck are you attempting to buy it now? Just go away and buy what you like somewhere else.” And then I actually get a desire to increase the price for this annoying person. Words “I’d rather dump it in the harbor than sell it to you” are a very accurate description of how I react whenever people start haggling with me.

Interestingly, I wouldn’t get so annoyed if the person attempting to haggle simply said things like, for example, “Could I get it cheaper? Pretty please. I really need it.” What really annoys me are people attempting to convince me that the stuff I’m selling is actually worth less than what I’m asking. Basically, they are implying that I’m too dumb to accurately estimate the value of some stuff.

While it certainly does take a big kick to move the market in the short term, I’m more concerned about the potential for market distortion caused by the compounding of relatively small, but constant, drips of investment over a long period. The whole principle of long term investing is that small percentage changes add up when compounded over long periods, so I’m reluctant to wrote such effects off without some serious quantative analysis, which AFAIK, nobody’s actually done. (Or made public anyway…)

It also seems at least possible that there’s potential for unexpected feedback effects once you get to the point where a significant proportion of all trades are being made by algorithms chasing each other…

Just made me think of this: The Markets.

It also seems at least possible that there’s potential for unexpected feedback effects once you get to the point where a significant proportion of all trades are being made by algorithms chasing each other…

That’s already happened, and still happening. Often it’s minor, harmless changes in quotations (can be fun to watch, a little like Conway’s Game of Life); other times it makes bad conditions much worse.

That’s true of not just pension funds but all savings that are not held as cash (whether under your mattress or elsewhere). But remember, all this money, in a country with a fiat currency, is just a made-up social construct, anyway. The government creates however much money it likes via issuing currency (which issuance in turn leveraged via fractional reserve banking and other mechanisms) and government spending and lending, injecting it into the economy, and removes that money via taxation and issuing government debt such as treasury bonds. Return on investment (interest or otherwise) would normally be reduced as demand for investments increases; this can be avoided by the government issuing debt to satisfy that demand (or by increasing taxes to reduce the demand). It’s also important to keep enough money on the economy to keep it easy to exchange money for labour, and so governments that want to do this will need to do spending and lending at times when private demand for investment can’t well satisfy this need. If they don’t, and thus someone willing to work doesn’t work for a day because nobody has the money to pay him, that day of labour and its contribution to the economy is lost forever.

So you can see that (again, emphasizing that this applies only in countries with fiat currencies) government “debt” is an entirely different animal from private sector debt and should definitely not be treated in the same way if you want a well-functioning economy. And you’ve now just learned a little bit about Modern Monetary Theory (MMT), which is fascinating and enlightening to learn about.

Lofty@#12:

link

Why did I not know of this thing? It’s great. Gilbert and Sullivan except educational! Thank you for sharing!